How Much Down Do You Need To Purchase

Joe Muck

As an entrepreneur and former co-owner of a successful residential moving company, Joe understands the importance of attention to detail and the art o...

As an entrepreneur and former co-owner of a successful residential moving company, Joe understands the importance of attention to detail and the art o...

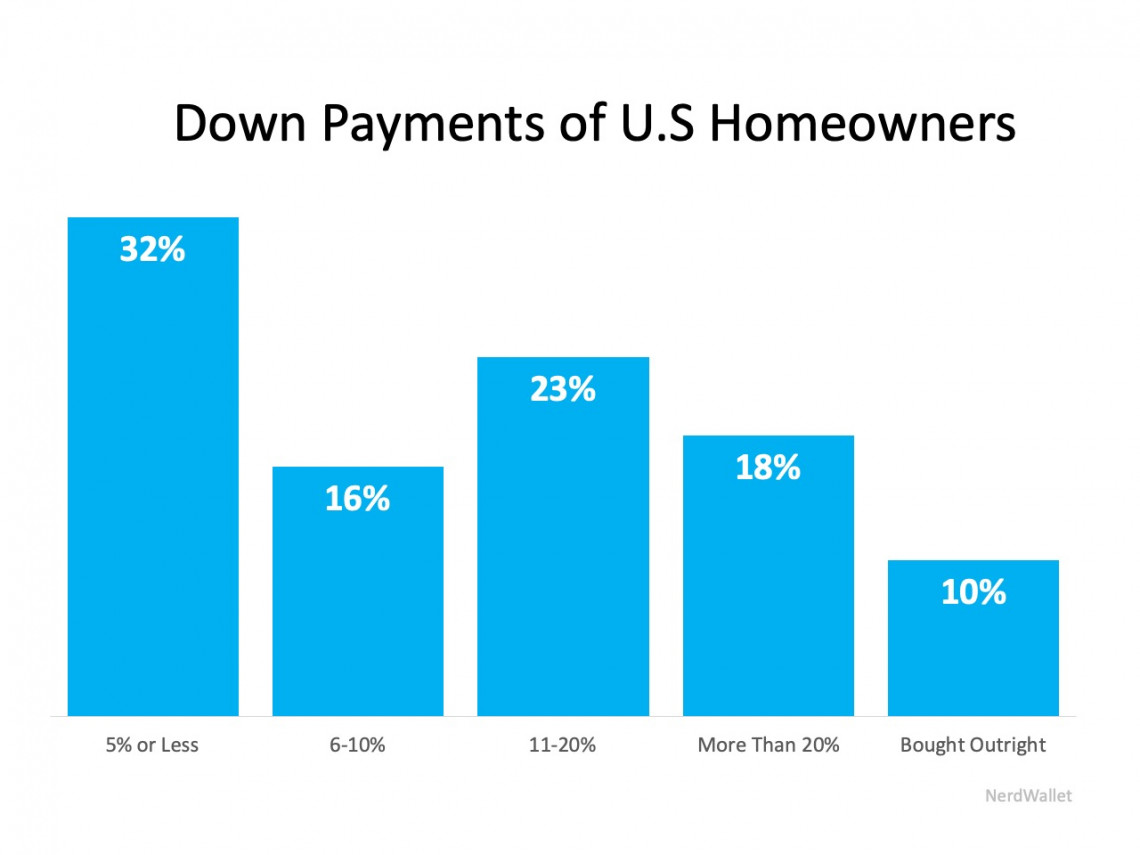

62% of buyers are wrong as to how much money down they'll need to buy a house. Many people still believe the old wive's tale of needing 20% down on their home purchase. The truth is, this answer is dependent on many circumstances and vary from person to person.

1. Credit Score.

One of the first indicators to how much money you'll need down is dependent upon your credit or FICO score. Some scores may be too low or even too high for various loan products. There are specific loans ranging from Veteran's only loans to Conventional to FHA and more. Don't get bogged down in the details of the loan product, names, and qualifications. Work with an experienced mortgage lender to help identify options for you.

2. Debt-To-Income Ratio.

DTI is also important. Again, amongst the multitude of loan products there are debt ratio qualifiers that may eliminate some of the options out there. This is closely tied to the credit score in many cases. FHA has one acceptable max debt ratio while Conventional loans is entirely different. Exceptions are sometimes made from underwriters if one of these factors is far superior to another one.

3. Assets.

Available funds are considered assets and often times called reserves. Depending on your circumstances, size and type of loan and much more, you may be required to have little to no assets or six months worth of reserves. What exact are reserves? Liquid funds (checking, savings, mutual funds and stocks that can be cashed in. Not IRA, educational funds, classic cars, etc) that can be used to make your mortgage payment in the event your usual income is interrupted an unable to be used at a particular time.